FEMA Flood Zones

Know them early, before flood insurance surprises you

Updated 2026-06-29

Flood risk can surprise California home buyers, but it is far from rare. Often it surfaces late, after you have already invested time and effort in a home you like. Then, in the worst case, at the loan review table, you are told you need flood insurance because the home sits in a Special Flood Hazard Area.

Most buyers don't know exactly what that means or what it costs. This article explains the basics so you can weigh this risk against your own preferences, ideally before you ever schedule the tour.

Key Takeaways

- A FEMA flood zone tells you the flooding risk at an address. The high-risk areas, the Special Flood Hazard Area (SFHA), are the "1-percent annual chance" floodplain, also called the base flood or "100-year flood."

- Flooding is "the most common and the most expensive disaster," and 90% of presidentially declared U.S. disasters involve flooding.

- Flood-related damage is not covered by standard homeowners insurance, and in an SFHA with a federally-backed mortgage, flood insurance is mandatory.

Being in a mapped zone is not necessarily a deal-breaker. It's a prompt to look closer, a strong factor to weigh against comparables, and a likely reason to negotiate.

What a FEMA flood zone actually is

The Federal Emergency Management Agency draws flood zones on Flood Insurance Rate Maps (FIRMs). The one to know is the Special Flood Hazard Area (SFHA). FEMA defines it as "the area that will be inundated by the flood event having a 1-percent chance of being equaled or exceeded in any given year. The 1-percent annual chance flood is also referred to as the base flood or 100-year flood." "100-year flood" is a confusing name: it doesn't mean once a century. It means a 1-in-100 (1%) chance every single year.

The zone codes look cryptic but boil down to a few categories:

- A, AE, AH, AO, A1–A30: high-risk inland SFHA. "Zone AE indicates areas that have at least a 1%-annual-chance of being flooded." (AO is shallow sheet flooding, AH is shallow ponding, plain A means no detailed base flood elevation was calculated.)

- V, VE: high-risk coastal SFHA. "Zone VE, also known as a Coastal High Hazard Area, is where wave action and fast-moving water can cause extensive damage during a base flood event."

- X (shaded) / B: moderate risk, "usually between the limits of 100-year and 500-year floods."

- X (unshaded) / C: minimal risk, above the 500-year flood level.

- D: "areas where flood risk has not been determined." Undetermined is not the same as safe.

Why it matters in California

In California, flood exposure is enormous, and not only on the coast. The Department of Water Resources notes that "millions of Californians are at risk from flooding along thousands of miles of streams, rivers, lakes and coastline," and that in many leveed areas "the risk of flooding is greater than the risk of fire." Cal OES adds that you should "be aware of flood hazards no matter where they live… as even very small streams, gullies, creeks, or dry streambeds can flood."

FEMA flood zones are not the complete answer. Being outside a high-risk zone is not the same as zero risk. FloodSmart reports that from 2014–2024, nearly one-third of NFIP flood claims came from areas outside the mapped high-risk zones, and in 2024 alone $3.8 billion in flood damage hit communities not considered high-risk.

How to read it for a specific address

FEMA's flood data is public, and home buyers can reach it through official, free tools:

- FEMA Flood Map Service Center (MSC): "the official public source for flood hazard information produced in support of the National Flood Insurance Program." Type an address; it returns the FIRM and the property's flood zone, drawn from the National Flood Hazard Layer. → msc.fema.gov

- Cal OES MyHazards: California's tool "for the general public to discover hazards in their area (earthquake, flood, fire, and tsunami)." Enter an address, city, or ZIP. → myhazards.caloes.ca.gov

- The disclosure (NHD) statement: California's Natural Hazard Disclosure (Civil Code §1103.2) has a checkbox for a "SPECIAL FLOOD HAZARD AREA (Any type Zone 'A' or 'V')" and one for an "AREA OF POTENTIAL FLOODING" (dam-failure inundation), each answered Yes / No / "Do not know."

Two caveats that matter. First, maps get revised, and FEMA's MSC warns that flood maps are continuously updated, so an old printout "may be superseded by newer maps." Second, as above, out-of-zone ≠ no risk. A zone is a flag for a closer look, not a verdict.

What it costs

Insurance, the part that surprises people. Standard homeowners insurance "excludes flood damage." Flood is a separate policy, usually through FEMA's National Flood Insurance Program (NFIP). And in a high-risk zone, it's not optional: "under federal law, the purchase of flood insurance is mandatory for all federal or federally-related financial assistance for the acquisition… of buildings in high-risk flood areas." If the home is in an SFHA and you have a federally-backed mortgage, you carry flood insurance for the life of the loan. FEMA now prices it under Risk Rating 2.0, which rates each property to its own flood risk rather than to the zone alone.

Don't count on disaster aid instead. FEMA's own numbers: between 2016 and 2022, the average FEMA disaster grant was $3,000, while the NFIP paid an average claim of more than $66,000, and grants only flow after a presidential disaster declaration. Insurance pays regardless.

Mitigation. For homes that face real exposure, FEMA's Protect Your Property From Flooding guidance covers elevating the structure and utilities (furnace, water heater, electrical panel), installing flood vents, and improving grading and drainage, investments that can also lower the premium.

How to deal with it

If a home you love sits in (or near) a flood zone, here's the playbook:

- Check early. Pull the flood zone before you tour (FEMA MSC, Cal OES MyHazards, or OpenHomeVue).

- Read the disclosure. Confirm the SFHA and area-of-potential-flooding checkboxes on the NHD statement, and request the flood-zone determination.

- Get the right paperwork. An Elevation Certificate (prepared by a licensed surveyor or engineer) documents the building's elevation and sets the insurance rate. If a home was mapped into the floodplain but actually sits on high ground, a Letter of Map Amendment (LOMA) can officially remove it from the SFHA, and remove the lender's insurance requirement.

- Mitigate. Elevate utilities, add flood vents, fix grading and drainage.

- Insure deliberately. Price the NFIP premium into your budget from the start. In an SFHA with a federally-backed loan, you're carrying it anyway.

How OpenHomeVue helps

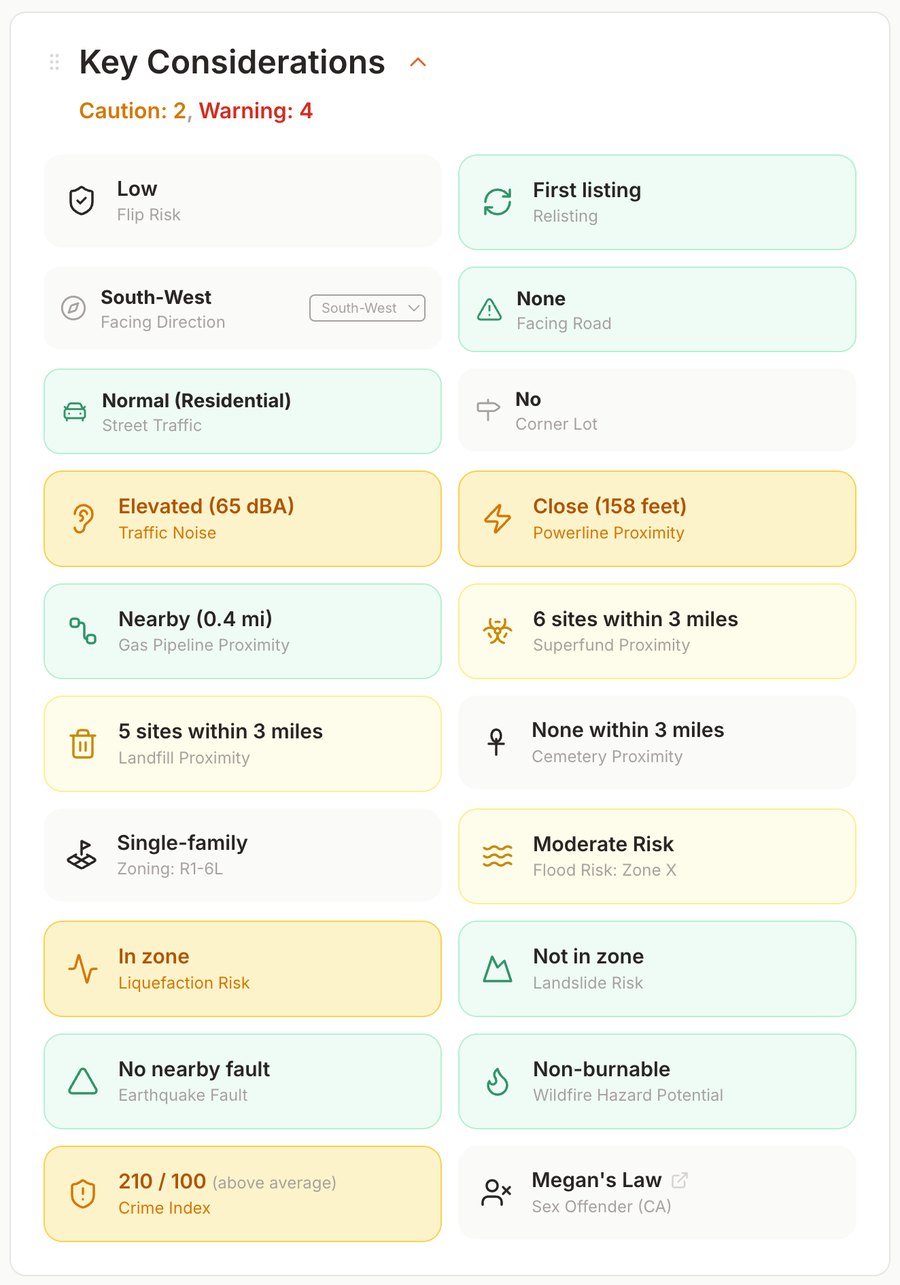

OpenHomeVue pulls the same authoritative FEMA flood data, the National Flood Hazard Layer, and turns it into a plain-language Flood Risk chip on every property you're considering. It shows the property's actual FEMA flood-zone code (for example, Zone AE), flagged in red when the home sits in a Special Flood Hazard Area. Where FEMA doesn't return data for the parcel, we say "No data" rather than implying "clear."

Every property gets a Key Considerations card; here the Flood Risk chip flags Moderate Risk (Zone X) at a glance.

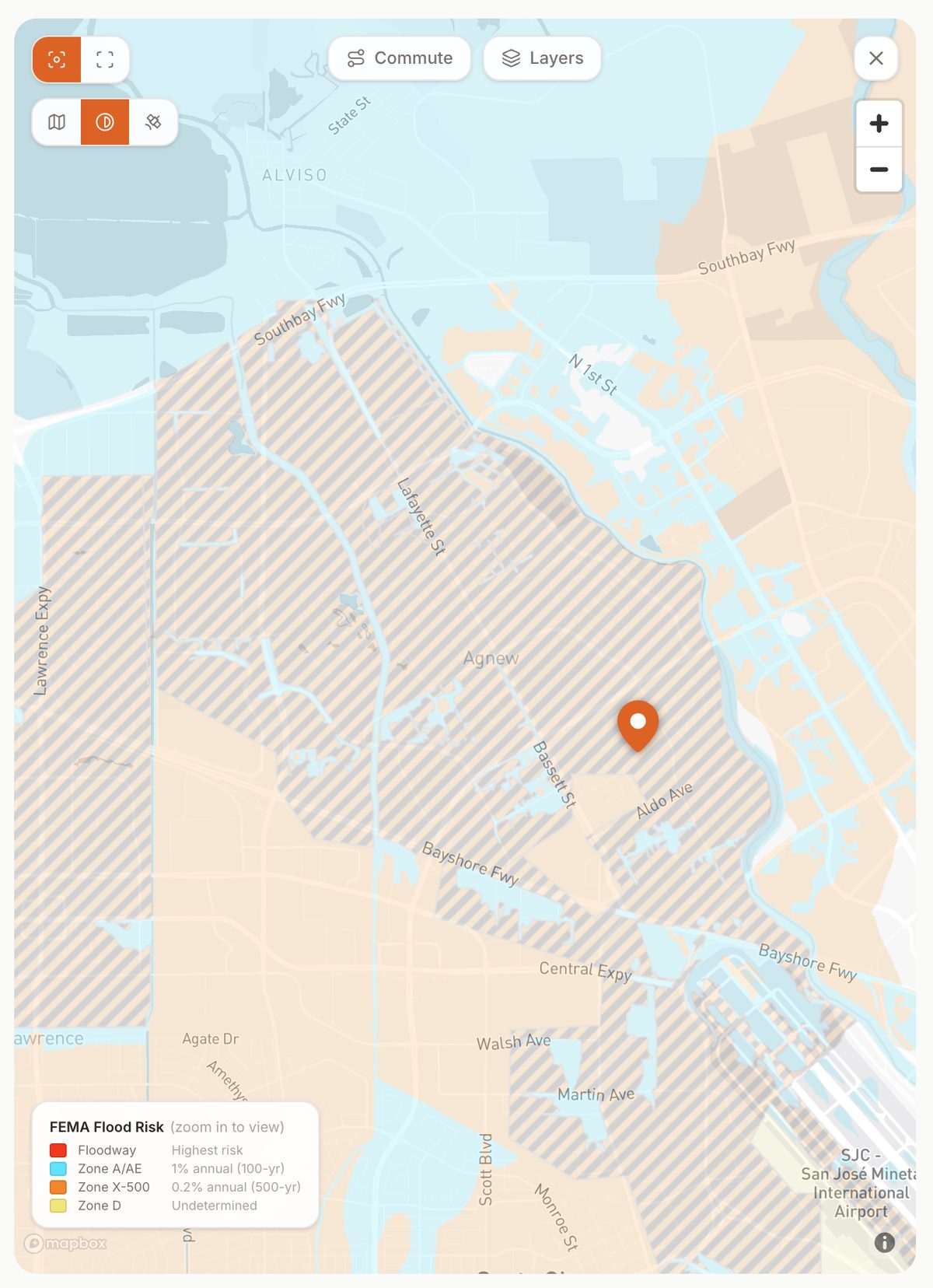

There's also a map overlay that renders the FEMA flood zones right around the property, so you can see whether the house is in the zone or just near its edge. The difference from a disclosure packet is when and where you see it: not a checkbox you discover at closing, but a status on the map, on day one, across your entire watch list.

The same property's FEMA flood zones on the map overlay, so you can see whether the home sits inside a mapped zone or just near its edge.

Sources

- FEMA, Flood Zones (glossary)

- FEMA, Special Flood Hazard Area (SFHA)

- FEMA, Flood Insurance / National Flood Insurance Program (NFIP)

- FEMA, Flood Map Service Center (official public source / National Flood Hazard Layer)

- FEMA, The NFIP's Mandatory Purchase Requirement

- FEMA, Risk Rating 2.0: NFIP's pricing approach

- FEMA, Protect Your Property From Flooding (home mitigation guidance)

- FEMA, Everyone Needs Flood Insurance (avg claim vs. disaster grant)

- FEMA, Letter of Map Amendment (LOMA)

- FEMA, Elevation Certificate

- FloodSmart (NFIP), What is my Flood Zone

- FloodSmart (NFIP), What is My Flood Risk (~1-in-3 claims outside high-risk areas)

- FloodSmart (NFIP), The Cost of Flooding (most common & costly disaster)

- Cal OES, MyHazards

- California Department of Water Resources, Flood Risk Notification / My Flood Risk

- California Civil Code, §1103.2, Natural Hazard Disclosure Statement

All sources are U.S. federal (FEMA / NFIP) or California state (Cal OES, DWR, California statute) government sources.